FX Daily Strategy: Asia, April 17th

GBP could benefit from higher than expected CPI…

…but we still see upside as very limited given current pricing of rate cuts

JPY in focus as weakness continues

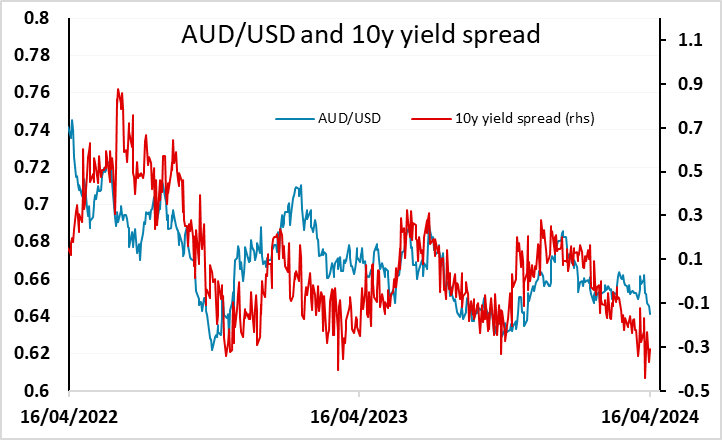

AUD looks to have further downside risk

GBP could benefit from higher than expected CPI…

…but we still see upside as very limited given current pricing of rate cuts

JPY in focus as weakness continues

AUD looks to have further downside risk

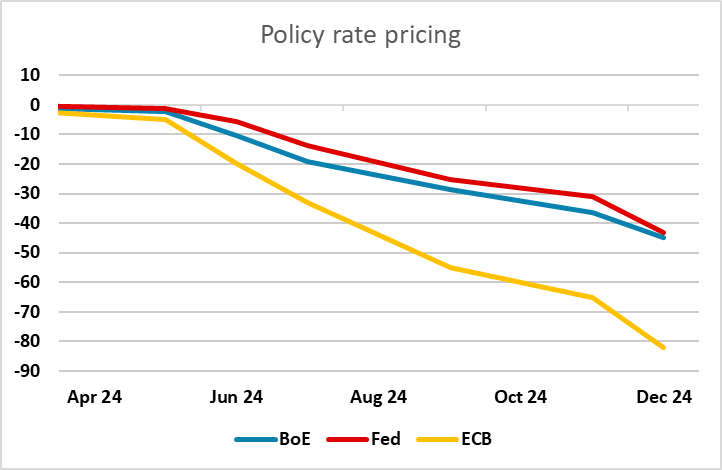

UK CPI is the main calendar item for Wednesday. UK yields rose on Tuesday, even though the UK labour market data was at best mixed. While earnings growth was a tad higher than expected, earnings remain near flat since November so the latest data will not be a concern to the Bank of England. Meanwhile, the employment data were clearly weak, both in the ONS and the HMRC data, and the unemployment rate rose. The renewed rise in inactivity was a concern, and may make the BoE less sure that weak employment growth will lead to lower earnings growth, but the rise in UK yields seen on Tuesday nevertheless doesn’t look justified. This means there might be scope for yields to decline on the CPI data, which is expected to show another fall in the y/y rate to 3.1% with core down to 4.1%. However, we see a slightly smaller decline than the consensus, and if there is still evidence of strong service sector inflation, the market may still shy away from pricing in a UK rate cut before H2.

Currently, the first UK rate cut isn’t priced until September, which lags behind the likely ECB stance. Lagarde and others spoke on Tuesday indicating that a rate cut as likely in June barring surprises. There is an opportunity for BoE governor Bailey to indicate where the MPC stands as he speaks on Wednesday evening. The risks should be towards the GBP rate cut path moving more towards the EUR and away from the USD, given the economic correlations. So even though the CPI data may trigger a downside test for EUR/GBP, we would doubt that there will be progress 0.85.

Elsewhere, eyes are still on the JPY which weakened against the USD and EUR on Tuesday (although the AUD was even weaker). USD/JPY dipped sharply just after the US equity market open at 14:30, losing nearly a big figure, but at this stage there is no evidence that the decline was a consequence of BoJ intervention. Equities also fell at the open, and we saw weaker commodity currencies as well, so the JPY rise might just reflect risk averse trading. Even so, we are at levels that should make markets nervous about potential BoJ action. The JPY is at extremely low levels – real terms lows in the floating era – and BoJ intervention has typically been effective at extremes. There have been plenty of warnings from the Japanese authorities, and if they allow a break above 155 in USD/JPY and 165 in EUR/JPY without acting, they will lose credibility. So although this dip doesn’t look like it is intervention related, it is a warning about the possibility.

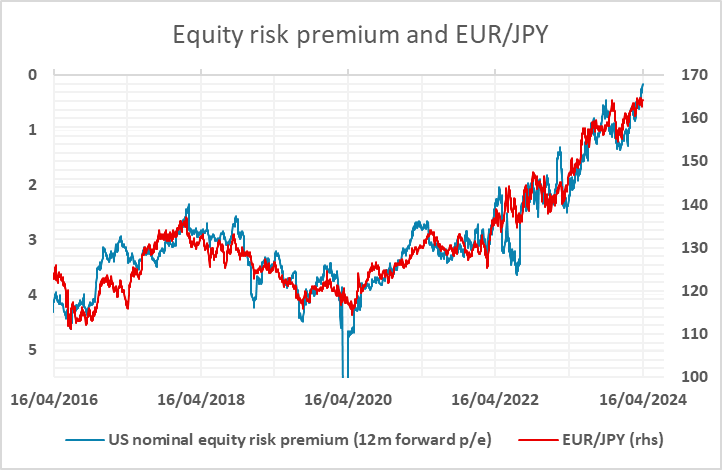

The weakness in the AUD was triggered by the decline in equities and the rise in US yields, and after the break through 0.6450 there looks to be potential to test the lows from last October below 0.63. While some of the equity weakness may be related to geopolitics, we would see it as primarily a consequence of higher US yields. Indeed, the nominal US equity risk premium is still very close to its lows since the GFC, supporting the weakness of the JPY. But the rise in US yields has led to a widening of spreads with the AUD suggesting further downside risk, and sentiment is not helped by weakening global equities.